How much debt is too much debt?

By some tellings, debt is as old as we are: our species emerged as such when relationships of informal indebtedness (you give me sheep, I’ll give you vegetables) allowed us to specialize our labor, which in turn kicked off the whole progress exponential we’re still riding.

Enforcing private debts may have been the original purpose of the state, per Graeber, though the theory is hard to falsify. Still, once you have private debts and a state to enforce them, why not let the state take on debt, too? From 377 to 373 BCE, thirteen states borrowed from the Delos temple (though only two honored the terms.)

Debt helps states do things, big projects that take time to pay off. The Ottoman Empire borrowed large sums from foreign powers, starting with the Crimean War in 1854, to finance railways and modernization (and to cover deficits from lavish court spending—if you detect modern parallels, trust your instincts).

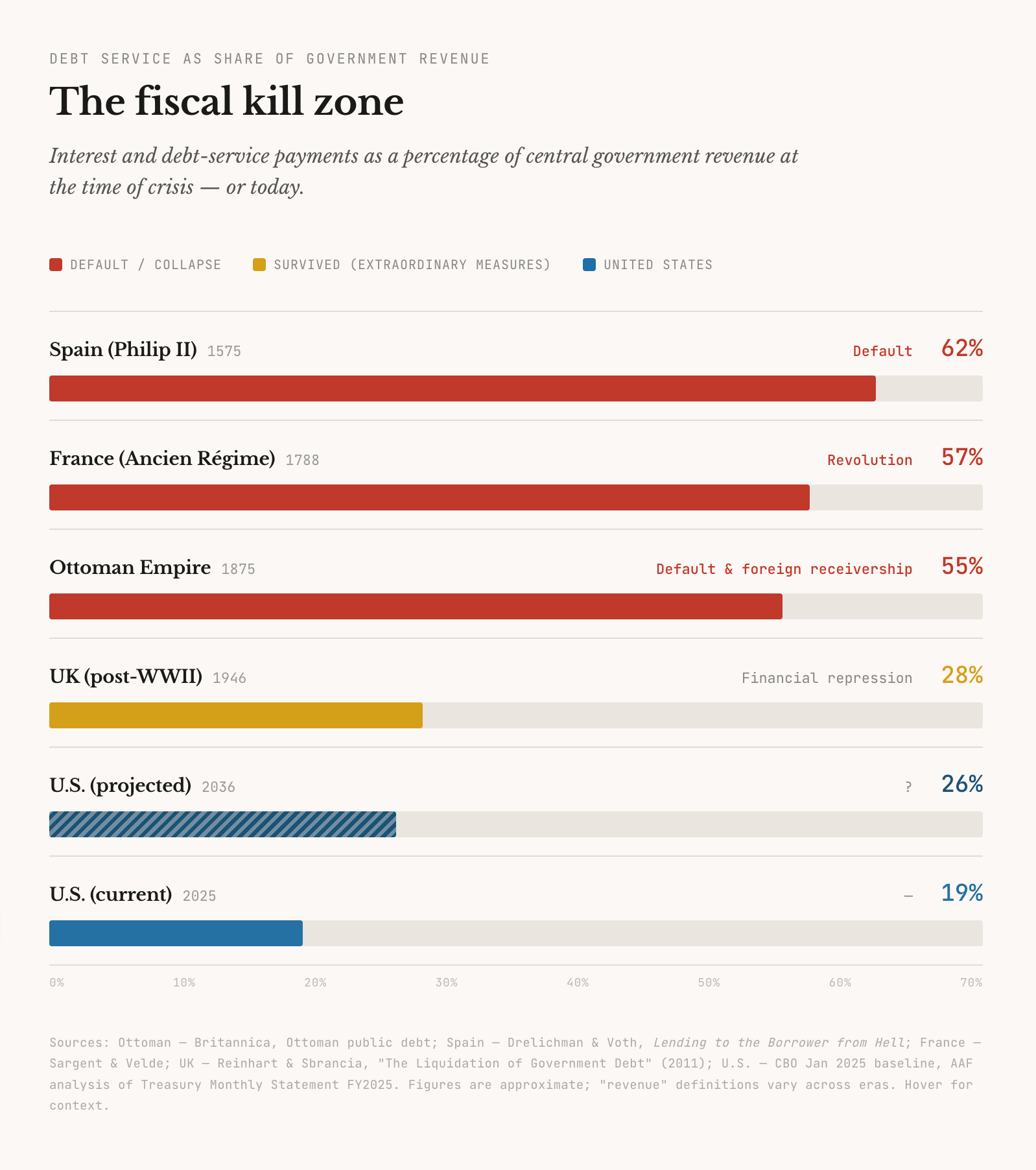

Excessive debt has ended states. By 1875, the Ottoman Empire owed ~10x revenue; annual payments on that debt consumed more than half of national revenue. The Empire suspended interest payments on loans. Foreign creditors created a foreign receivership, then the Ottoman Empire recovered and lived happily to this day (kidding about the last part).

Which brings us to the U.S. It’s easy to get desensitized, but the U.S.’s debt load is high:

And this high debt load is in the face of structural headwinds: an ageing population, expensive climate adaptation on the near horizon, and a rising geopolitical rival. Any of the three is expensive on its own.

So, how does the U.S. get away with taking out all this debt? A few reasons, not exhaustive. First, and most important, TINA—“There Is No Alternative”. No other debt market is as liquid as the market for U.S. treasuries. If you want to park some money, U.S. Treasuries are the obvious place, and there’s plenty of demand for money parking. With all this demand, why not create supply—that is, sell debt? The U.S. hasn’t exhausted this demand—yet, though some Treasury auctions have been weaker than normal.

Second, the U.S. uses quantitative easing (QE). The details1 will make your eyes glaze over, but in effect, Q.E. lets the government borrow at lower rates than it otherwise would by having the Fed step in as a buyer of Treasuries.

Third, the U.S. policy mix funnels money toward U.S. debt. Post-WWII, these mechanisms were overt. The current policy stack is sneakier,2 though there are hints it may get more overt again—the GENIUS act requires stable coins be 1:1 backed by treasuries or equivalent liquid dollar assets; if stable coins take off, the U.S. gets new demand, which lets it issue more debt! (The “cash” in your wallet or bank account is powered by fractional reserve banking—banks need much less than 1:1 reserves to give you a checking account).

So, what would make the U.S. stop getting away with taking on so much debt? The ultimate, if unsatisfying, answer is that they’d need to run out of buyers—or face a bond market revolt, in which existing holders scramble to sell off their U.S. treasuries.

There are a few reasons a supply-demand imbalance may arise, none mutually exclusive. On the demand side, the U.S. dollar’s status as the global reserve currency or preferred currency to settle accounts may weaken, in one or many sectors or geographies, relative to upstarts like EUR or RMB. That would suppress demand for USD-denominated debt. Regulatory dysfunction could spook investors, causing a sell-off (see: Truss). Foreign state-aligned entities, like central banks or public pension funds, could sell, or threaten to sell, their USD holdings as a geopolitical weapon. Not a pretty outcome for anyone, but in a pinch, it could be the least worst option.3

On the supply side, we know the U.S. will need to take on more debt to cover climate adaptation. An ageing population also adds revenue pressure, absent increased immigration (fewer young people means a lower share of the population pays income tax). And a war—a big one—could greatly increase the U.S.’s spending needs, which will need to be funded by… well, you get the idea. Depending on who that war is against (think: a state that owns lots of treasuries), a sudden supply/demand imbalance is well within the realm of possibility.

Finally, bond markets are self-fulfilling. If investors are worried enough about any of these possibilities, they will demand higher yields, which raises the deficit, which increases supply, which validates the worry.

What would happen then? I highly doubt the U.S. would default—unlike every scary example in the chart above, the U.S. borrows in its own currency. The U.S. can always pay its debt… in nominal terms. That is, the Fed would likely act to weaken the currency. Of course, that would drive inflation, which would hammer U.S. consumers, the engine of global demand. We’d be left with a poorer world, even if the Fed managed this devaluation smoothly.

Britain had to make similar moves after WWII. It used financial repression (effectively, encouraging citizens to buy its debt) to lower its debt-to-GDP ratio down to manageable levels over time. It never defaulted. But, sterling lost its reserve currency status. The empire dissolved. Living standards fell behind continental Europe. By 1976, Britain was borrowing from the IMF, the institution it had helped create.

In other words, the U.K. muddled through. Despite some truly hysterical reports to the contrary, the U.K. is neither facing imminent economic collapse nor is it a formerly developed country. It is merely European.

If the U.K. is a template, “too much debt” is probably not a catastrophic crisis. The likelier outcome is a slow transition from one type of country to another.

There is a difference, though. During Britain’s decline, the Sterling had a clear successor: the dollar. Better, a close ally issued it. What would be the dollar’s successor? RMB isn’t freely convertible. EUR is tricky—one monetary union, no single debt issuer; that is, no single safe asset for the world to pile into. If you're a central bank looking to park $500 billion, where do you go? Either TINA will hold, or any transition will be much bumpier than the U.K. analogy implies.

In QE, the Federal Reserve buys Treasury securities from banks using money it creates for the purpose. That demand pushes down the interest rate on Treasuries (more demand = lower yield). It also floods the banking system with reserves, which keeps broader borrowing costs low. The net effect is that the government can borrow more cheaply than it otherwise would. Between 2009 and 2021, the Fed purchased roughly $5 trillion in Treasuries this way. People with a Perspective will describe QE as “printing money,” which isn’t quite right: the Fed is swapping a Treasury liability (a bond) for a Fed liability (bank reserves). But the practical effect is similar: it lets the government fund itself without fully testing the market’s appetite. The Fed is currently reversing this process (”quantitative tightening”), selling bonds back into the market, though it has slowed the pace considerably — which could tell us something about how confident it is in the market’s ability to absorb supply.

After WWII, the U.S. and UK used a toolkit economists now call “financial repression”: interest rate caps (Regulation Q), capital controls, and explicit yield curve control by central banks. The effect was to hold interest rates below inflation for decades, gradually eroding the real value of the debt, effectively forcing slow-motion transfer from savers to the government. It worked: the U.S. went from 106% debt-to-GDP in 1946 to 23% by 1974 without defaulting. Today’s version is subtler. Bank capital regulations (Basel III) effectively require banks to hold large quantities of Treasuries as “risk-free” assets. Money market fund rules channel savings into government securities. The Fed’s own massive balance sheet absorbs supply. None of these policies are designed to prop up demand for government debt — they have independent regulatory justifications — but the cumulative effect is the same: domestic savings are quietly steered toward Treasuries at rates the market might not otherwise offer.

Worse, the Treasury has shortened average maturities in recent years, meaning debt rolls over more frequently. That makes the Treasury more vulnerable to rate spikes: if rates jump, new debt will be financed at those higher rates, which the U.S. would have to pay.

Hard times ahead; suggest gold, silver, farm real estate to weather the eventual inflationary storm.